What It Actually Costs to Buy a $1.05M Auckland Home

Date 29 May 2026

REINZ recently reported Auckland’s median house price at around $1.05 million.

That number can feel huge on its own, but for many buyers, the more important question is not just, “What is the purchase price?”

It is: What would I actually need to buy a home at that price?

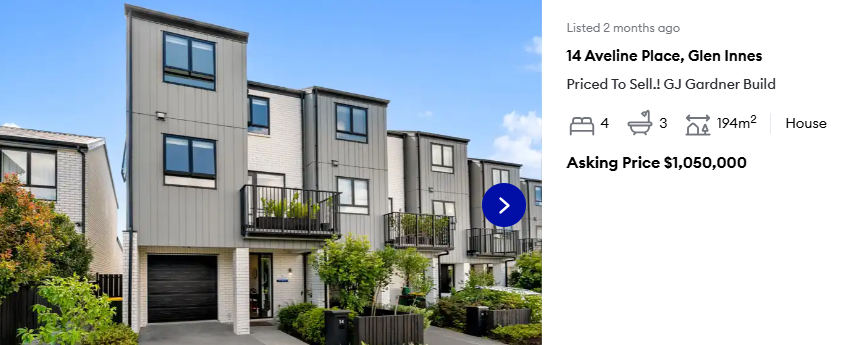

To make it easier to understand, let’s use an example: a $1.05 million, 4-bedroom, 3-bathroom home in Auckland.

The Deposit

If you are buying with a 20% deposit, you would need: $208,000 upfront.

That leaves you with a mortgage of approximately: $832,000.

For many buyers, this is the first big number to understand. The deposit is not the full cost of buying the home, but it is usually the largest upfront amount you need to have available.

In New Zealand, a 20% deposit is often used as a standard example because it usually helps avoid low-equity lending restrictions and can make the application stronger with the bank.

However, not every buyer will have 20%. Some buyers may be able to purchase with less, depending on their situation, lender criteria, income, debts, and the type of loan they are applying for.

The Mortgage Repayments

Using the example above, with a loan of around $832,000, and based on a 4.59% one-year fixed interest rate at the time of recording, over a 30-year loan term, the repayments would be approximately: $1,984 per fortnight.

This is the amount you would need to budget for your mortgage repayments.

However, it is important to understand that this number can change.

Your actual repayment will depend on things like:

- The interest rate available at the time you apply

- The loan term you choose

- Whether you choose weekly, fortnightly, or monthly repayments

- Whether you split your loan across different fixed or floating rates

- Whether you make extra repayments

Interest rates also move over time, so it is important not to only ask, “Can I afford this today?”

A better question is: Can I still afford this if my repayments increase later?

That is one of the reasons banks test your affordability at higher rates than the rate you may actually pay.

Other Upfront Costs

The deposit is not the only upfront cost.

When buying a home, you should also allow for other costs such as:

- Legal fees

- Building inspection

- Registered valuation, if required by the bank

For this example, a good estimate would be around: $3,500 to $4,000.

These costs can vary depending on the property, your lawyer, your lender, and whether additional reports are required.

It is easy to focus only on saving the deposit, but you do not want to use every dollar on the deposit and then realise you still need money for the buying process itself.

Ongoing Costs After You Buy

Home ownership is not just about getting the keys.

Once you own the property, you also need to think about the ongoing costs of maintaining it.

A simple rule of thumb is to allow around 1% of the property value per year for ongoing costs and maintenance.

For a $1.04 million home, that would be around: $10,400 per year or roughly: $200 per week.

This does not mean you will spend exactly $200 every week, but it is a useful way to budget. Some weeks, you may spend nothing. Other times, you may need to pay for repairs, maintenance, insurance-related costs, rates, or general upkeep.

The point is to make sure you are not only budgeting for the mortgage, but also for the cost of actually owning and looking after the home.

So, What Do You Need to Buy This Home?

Using this $1.05 million Auckland home as an example, you would need to think about:

$208,000 deposit

Based on a 20% deposit.

$3,500 to $4,000 in upfront buying costs

This includes things like legal fees, building inspections, and valuations.

Around $1,984 per fortnight in mortgage repayments

Based on a $832,000 loan, a 4.59% interest rate at the time of recording, and a 30-year loan term.

Roughly $200 per week set aside for ongoing costs

Based on the 1% per year rule of thumb for maintenance and ownership costs.

The Real Cost of Home Ownership

The key takeaway is this: Buying a home is not just about the purchase price.

A $1.05 million home does not simply mean you need to think about $1.05 million. You need to understand the deposit, loan size, repayments, upfront costs, and ongoing costs.

That is where proper planning makes a big difference.

Before making an offer, it is worth sitting down and working through the numbers properly so you know what is realistic, what the bank may be willing to lend, and what repayments could look like for your situation.

Watch this video by our director, Mils Muliaina, as he breaks down what it actually costs to buy a $1.05 million home in Auckland.

And if you would like us to run the numbers for your situation, send us a message.

Our advice is free.

What else is happening in the market?

A snapshot of current articles relating to the housing market, interest rates, most popular areas to buy in and common trends relating to the property world in New Zealand.